Insights and inspiration from our community.

Understanding the drivers of insurance costs: the role of construction inflation

This is the first post in a series about drivers of pricing and availability in property insurance markets in the United States. An often underappreciated driver of premiums is the cost of construction, which is influenced by many macroeconomic factors. In recent years construction costs have risen substantially due to a confluence of compounding pressures.

Funding Climate Resilience: Trust, Enabling Conditions, and the Questions That Remain

This is the fifth installment in a blog series from CA FWD and Insurance for Good. This blog summarizes key themes from recent discussions by the expert workgroup convened through the partnership.

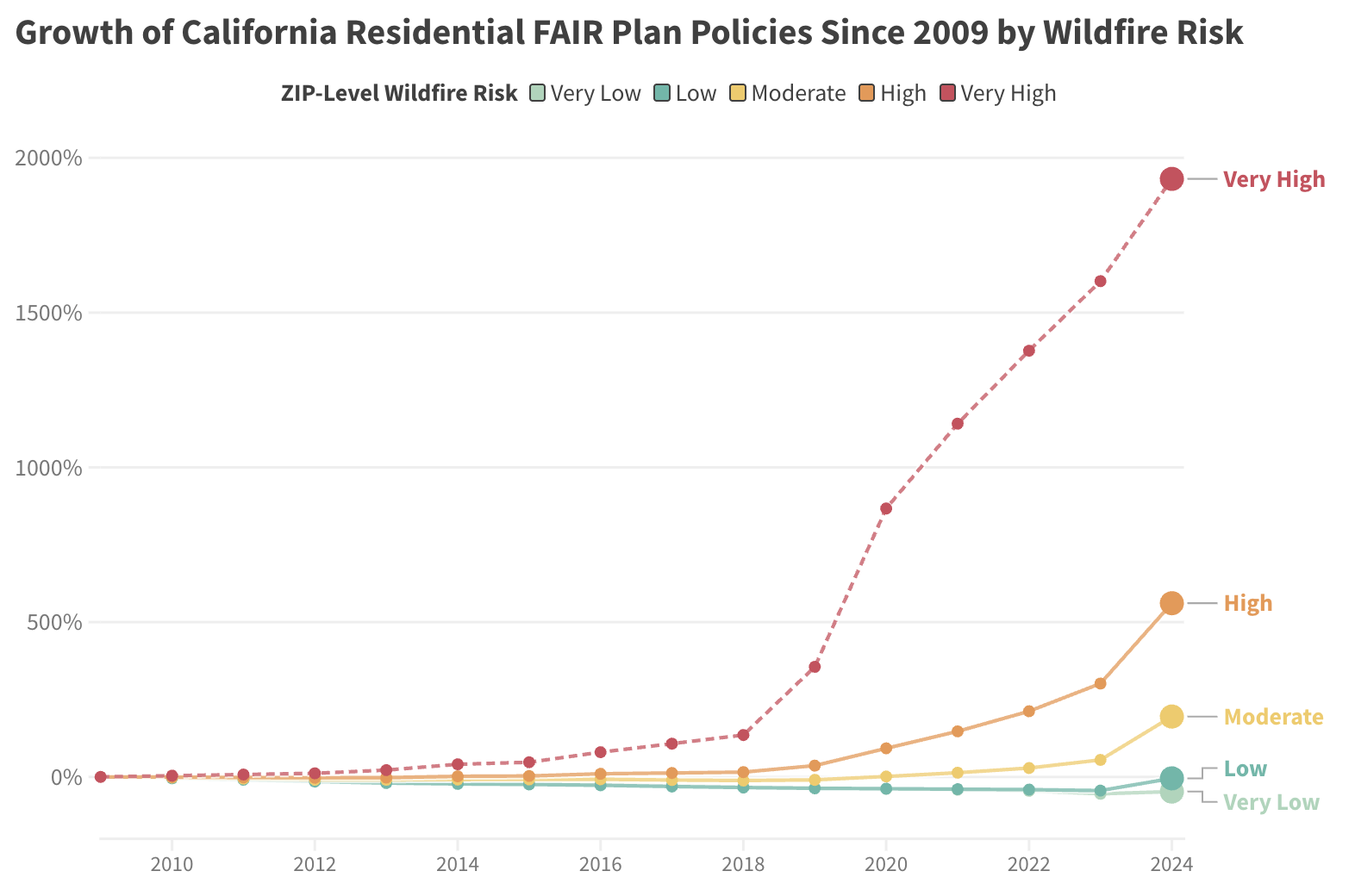

Exploring the Recent Growth in the California FAIR Plan

Growth in the FAIR plan has been substantial since 2018 and only recently, in the last quarter of 2025, has shown signs of slowing. This post explores how the growth in policies have varied by wildfire risk level and geography.

Why Resilience Finance Starts with Predevelopment

This is the fourth installment in a blog series from CA FWD and Insurance for Good. This guest contribution from PRE Collective covers how and why resilience finance begins with predevelopment.

California Can’t Afford to Wait: The Fiscal Case for Sustained Resilience Investment

This is the third installment in a blog series from CA FWD and Insurance for Good. This post outlines that California cannot keep pace with the costs of climate risk without a more stable and sustained approach to resilience investment.

Partnership Announcement: Launch of the Insurance Resilience Planning Program

Insurance for Good and the California Department of Housing and Community Development are pleased to announce the launch of the Insurance Resilience Planning Program (IRPP), in close coordination with the California Department of Insurance. Learn more about this partnership and new program for eligible communities in California.

Encouraging Property Insurers to Invest in Communities

Insurers manage a large amount of investments – nearly $9 trillion in the US alone. Our new blog explores how California and Massachusetts have encouraged insurers to invest in social and environmentally-friendly projects. The California Organized Investment Network (COIN) uses a voluntary approach to connect insurers to low-income and rural community development projects,. In Massachusetts, the Life Initiative (TLI) and the Property & Casualty Insurance Fund (PCI) directly invest insurer capital to provide early-stage funding to community development projects that might otherwise not attract sufficient investment.

Protecting Homes and Building Trust: OneShoreline’s Home Protection and Insurability Initiative

The community of Belle Air in San Bruno, California has a long history of flooding. To address this threat, a team of community partners led by OneShoreline, a regional government agency, is empowering residents through a low-cost, household-level approach to flood resilience. By reducing the impacts of chronic flooding at both this household scale and at the community scale, OneShoreline is working to lower uninsured flood losses.

Risk Ownership in a Time of Rising Climate Costs: Rethinking Who Pays, Who Benefits, and How We Move Forward

This is the second installment in a blog series from CA FWD and Insurance for Good. This post outlines the challenges of realigning responsibility, incentives, and investment so that resilience becomes the logical—not the exceptional—investment.

Funding and Financing Options for Resilience Investments

This is the first installment in a blog series from CA FWD and Insurance for Good. This blog summarizes the key themes coming from recent discussions by the expert workgroup convened through the partnership.

Do California Insurers Reward Wildfire Resilience?

In 2022, California implemented regulations requiring homeowners insurers to adopt premium discounts for policyholders who take steps to lower the risk of a wildfire burning their home. In this essay, we examine how California insurers have responded to these new regulations and summarize the premium reductions available currently in the California market. If homeowners adopt both the maximum home hardening upgrades and defensible space, the greatest premium discount they will receive varies from only a few percent to over 40 percent depending on the insurer and the loss reduction standards adopted.

Resilience Credits for FM Clients: Q&A with Joe Dimitriadis

In October, FM, an industrial and commercial mutual insurance company, announced $400 million in credits for existing policyholders to improve resilience and increase renewable energy use. The resilience credit was FM’s third in three years, providing a total of over $1 billion in premiums offsets to help clients protect their businesses against natural hazards. Insurance for Good sat down with Joe Dimitriadis, Vice President and Client Service Manager at FM, to hear more.

5 Ways to Better Link Risk Reduction and Insurance

Insurance for Good and CA FWD are launching a new partnership to develop durable funding and financing models for resilience. This work was launched with a joint dialogue that highlighted the resilience imperative and the tight link between risk levels and insurance market outcomes. Carolyn Kousky and Nuin-Tara Key share their takeaways.

New Wildfire Resilience Insurance in Tahoe Donner: Q and A with Dave Jones

An innovative insurance product was recently piloted in Truckee, California. The Nature Conservancy, Willis Towers Watson, and the Climate Risk Initiative at the UC Berkeley Center for Law, Energy, & the Environment collaborated on an effort to help insurance take account of nature-based efforts to lower wildfire risk. Insurance for Good sat down with Dave Jones, the Director of the Climate Risk Initiative, to discuss the wildfire resilience insurance product written for a community in the forest.

Building Wildfire-Resistant Homes After Disasters with Headwaters Economics

Insurance for Good partnered with Headwaters Economics to answer three questions: (1) How much economic loss could be avoided by building homes to wildfire-resistant standards? (2) What level of financial investment is needed to build wildfire-resistant homes following disasters? And (3) What types of programs could help homeowners afford the necessary upgrades?

Managing Risk from Good Fire: Prescribed Fire and Liability Insurance

Photo Credit: Steve Rondeau, Nature Resources Director for the Klamath Tribes. Prescribed fire is an essential part of reducing risk from catastrophic wildfires and improving ecosystem health. One of the barriers to expanding use of this important tool is the availability and cost of prescribed fire liability insurance, which has become increasingly harder to get.

Summary of Risk Mitigation Approaches Adopted by Residual Insurance Programs

State residual insurance markets have many tools to help lower the risk of disaster damages to their policyholders. This table summarizes the approaches taken by select programs.

Suggested Insurance Reforms in California to Create Resilient Communities and Inclusive Markets

Carolyn Kousky shares policy recommendations to reform the California insurance market with the Blue Ribbon Commission on Climate Action and Fire Safe Recovery. Her suggestions focus on creating insurable communities and inclusive insurance systems.

Lessons from the Isleton, CA Community Based Flood Insurance Pilot

Image: Isleton, California in 2024. (Alysha Beck/UC Davis) As many communities, small and large, face ongoing and increasing risk of flooding, new approaches to help residents prepare and recover are becoming increasingly important. The City of Isleton, CA is taking an innovative approach.

Puerto Rico’s Innovative Use of Parametric Insurance

To better protect itself and ensure a faster recovery, Puerto Rico, in partnership with FEMA, has taken a bold step by securing a parametric insurance policy as another tool in the toolbox to support pre- and post-disaster hurricane and earthquake recovery efforts.