Protecting Homes and Building Trust: OneShoreline’s Home Protection and Insurability Initiative

By Tai Michaels

The community of Belle Air in San Bruno, California has a long history of flooding. To address this threat, a team of community partners led by OneShoreline, a regional government agency, is empowering residents through a low-cost, household-level approach to flood resilience. By reducing the impacts of chronic flooding at both this household scale and at the community scale, OneShoreline is working to lower uninsured flood losses.

Flooding in the Belle Air neighborhood [OneShoreline]

Managing Flood Risk in San Mateo County

Officially named the San Mateo County Flood and Sea Level Rise Resiliency District, OneShoreline is a special district formed by state law in 2019 to build long-term resilience to climate change impacts in a county highly vulnerable to flooding and sea level rise. As the risk of extreme floods and fires increases, it is also stressing insurance markets. Nationwide, there has been concern about growing flood insurance premiums that are also failing to keep up with rising risks. And in the high fire risk areas of California, insurers have been pulling back, driving more residents into the state’s FAIR Plan. In San Mateo County, while the number of households in the FAIR Plan remains fairly low–under 4,000–it has been growing rapidly. Statewide, between 2020 and 2025, the number of residential policies in the FAIR Plan grew by a little over 200%, but in San Mateo County, it grew by over 700%.

To address these insurance challenges, OneShoreline launched the Home Protection and Insurability Initiative in late 2025. The initiative, in partnership with Insurance for Good, focuses on ensuring that climate resilience efforts translate into greater insurance access and affordability. OneShoreline is establishing pilot projects across the county that tackle flood and fire risk at the property and community scales. The Belle Air project is one such pilot, testing whether low-cost interventions, tailored to the needs of each home, can provide meaningful risk reduction for residents.

Belle Air

![FEMA flood map of Belle Air [FEMA NFHL]](https://images.squarespace-cdn.com/content/v1/629aa6f68914ce47a1d72993/f796c198-dd54-4de4-b102-985ac1461574/belle+air.png)

FEMA flood map of Belle Air [FEMA NFHL]

Belle Air is a low-lying, relatively low-income neighborhood in the city of San Bruno, California. It is bordered by San Bruno Creek, close to where it meets San Francisco Bay. Heavy rainfall, as well as storm surges and high tides from the Bay, can overwhelm the aging stormwater infrastructure and cause significant street flooding, most recently in 2021 and 2022. Flood risks in this neighborhood are anticipated to worsen due to more intense storms and sea level rise caused by climate change.

The vast majority of residential flood insurance is provided through the federal National Flood Insurance Program (NFIP), housed in the Federal Emergency Management Agency (FEMA). FEMA maps designate the Special Flood Hazard Area. By federal law, owners with a mortgage from a federally backed or regulated lender are required to purchase flood insurance. Many homes in Belle Air were added to FEMA’s Special Flood Hazard Area in 2019, expanding the number required to carry flood insurance. Despite this, less than half of Belle Air’s residents have a flood policy. Many households forgo flood insurance due to the added cost.

OneShoreline has managed this floodplain since 2019, inheriting responsibility from the former San Mateo County Flood Control District. The district owns and operates two pump stations and tide gates. OneShotline is also working on a larger flood mitigation project for San Bruno Creek. However, securing lasting solutions has proven challenging. Comprehensive flood management infrastructure is expensive and takes years to plan, permit, and build. Furthermore, the creek and the land surrounding it are owned by multiple agencies and entities, complicating any potential action.

Engagement

Since January 2024, OneShoreline and its partners have undertaken in-depth engagement with the Belle Air community to better understand their challenges and potential solutions. OneShoreline nucleated a team which included Stanford University researchers, the nonprofits Climate Resilient Communities (CRC) and Rise South City, regional government staff, and Community Leads—long-time Belle Air residents who are trusted by their neighbors. They met residents where they were through door-to-door outreach and one-on-one listening sessions conducted in both English and Spanish. They relied on CRC, Rise South City, and the Community Leads’ strong preexisting ties to the Belle Air neighborhood and its Latine community, helping extend their outreach to residents who might not otherwise engage with a government agency. “[The outreach] really helped establish the trust that … we actually care about their problems and are here to help,” said Stephanie Lau, Grant and Communications Advisor for OneShoreline.

One thing that stood out from these conversations was that residents wanted more immediate action. Across three workshops and more than 80 one-on-one conversations, OneShoreline and its partners heard story after story of mold, damaged cars, and destroyed belongings—not just from one flood, but from flooding year after year. OneShoreline entered the process more focused on long-term infrastructure solutions, and they successfully applied for a FEMA grant for planning and design in 2024. However, community conversations highlighted the need for immediate relief, especially with the uncertainty of future funding. “We were so focused on the long term planning that we weren’t thinking about short term relief for people early on—getting that balance right is important,” said Lau.

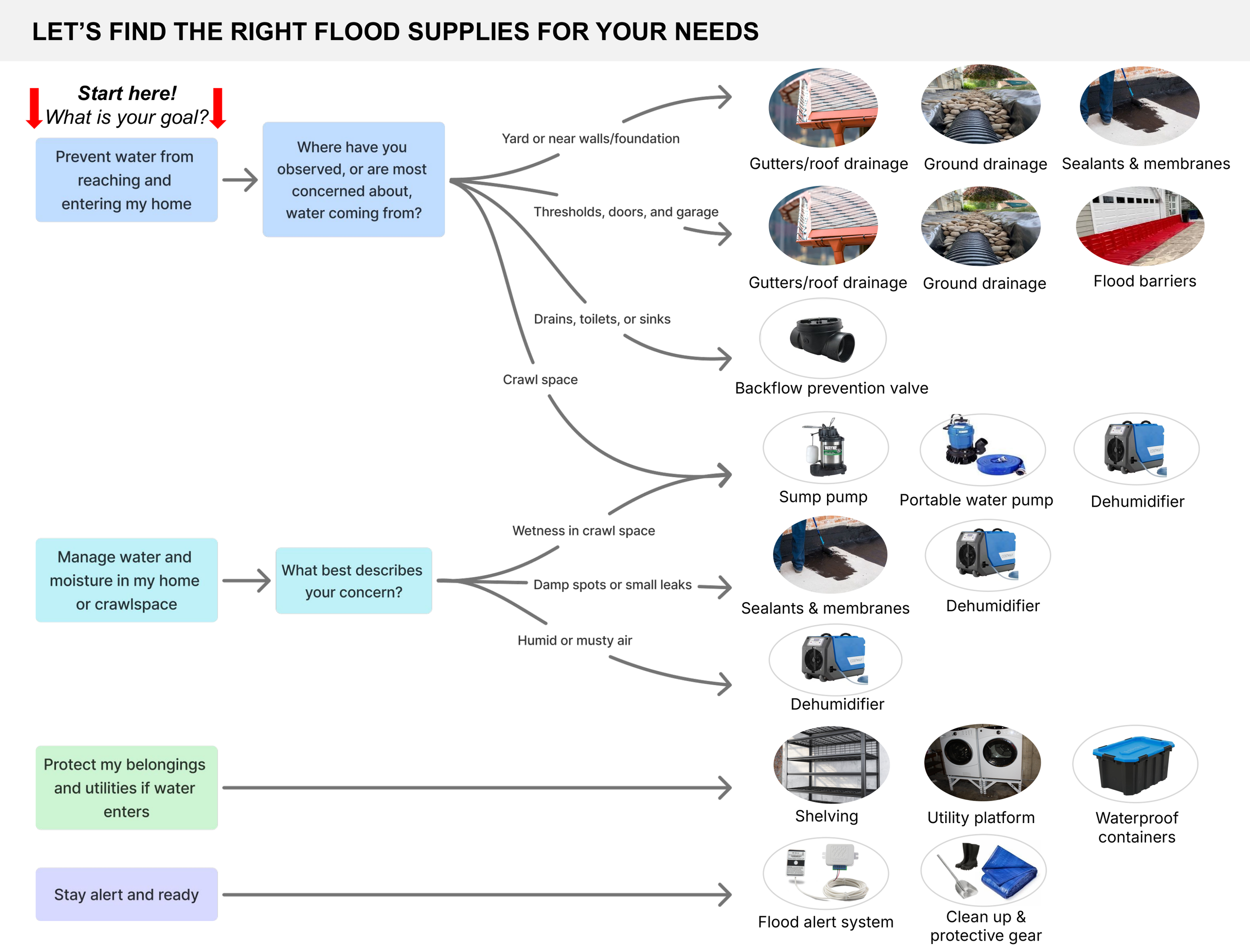

Microgrant program

Recognizing the importance of more immediate action, OneShoreline developed a microgrant program in 2025 to support household-level flood mitigation. OneShoreline and its partners identified a range of low-cost flood prevention measures such as sump pumps and garage flood barriers. Eligible households with the highest flood risks were offered grants of up to $1,500 to purchase flood protection supplies. OneShoreline’s partners promoted the program through flyering and door-to-door canvassing. Next, they worked with interested households to identify the best flood prevention methods for their homes based on home assessments and their experiences with flooding. With $50,000 in initial funding from OneShoreline, as well as $7,500 from Stanford University, the program has enrolled 29 Belle Air residents over its first winter.

Decision tree of flood control supplies. Image courtesy of OneShoreline.

This past winter, the program has enrolled more than 20 households, and the team has delivered the supplies to more Belle Air residents. In the coming months, the team will conduct surveys to assess residents’ experiences with the program and devise future improvements. If all goes well, OneShoreline is open to continuing and expanding the program. At the same time, they are weighing how to divide their resources between short-term, household-scale programs and long-term, community-scale flood management solutions. As part of OneShoreline’s FEMA-funded study, they are evaluating various priority infrastructure projects and will begin collecting community input this spring.

Reflecting on all of OneShoreline’s efforts in Belle Air, Lau emphasizes the importance of relationship building. Meeting residents one-on-one was crucial for building trust. Too often, formal community meetings are logistically or linguistically inaccessible, so it was important to meet people where they were. Leaning on community-based organizations (CBOs) for outreach was crucial to this. “There’s a lot of subtlety of interactions that a CBO can do much better than an agency,” said Lau, especially for non-English speaking neighborhoods. She also emphasized the importance of being flexible—while OneShoreline’s initial outreach efforts were focused on identifying long-term solutions, conversations with residents revealed the need for immediate, tangible actions. By listening and adapting its approach, OneShoreline was able to respond to community priorities while continuing to work toward long-term solutions.

I4G is pleased to partner with OneShoreline through our Solutions Catalyst. Learn more here.