Understanding the drivers of insurance costs: the role of construction inflation

This is the first post in a series about drivers of pricing and availability in property insurance markets in the United States.

By Xuesong You and Carolyn Kousky

The financial stress of rising household expenditures has been attracting increasing concern. Stagnating real wages, growing inequality, macroeconomic disruptions that impact labor markets and supply chains, as well as periodic inflationary pressures have collectively eroded purchasing power. The cost of living, including not just goods, but the costs of housing, including energy and insurance bills, have become a source of stress for households and stakeholder groups working to ease financial pressures. This backdrop explains the growing media and policymaker attention to the costs of property insurance, which, in recent years, has become a mainstream economic and political issue.

In unadjusted terms, the cost of property insurance has indeed been growing around the country. According to data from Keys and Mulder (2025), the average property insurance premiums paid by homeowners have increased by 52% from 2019 to 2024. This includes homeowners insurance and, if applicable, flood insurance required by lenders, the total cost of which is inferred from mortgage escrow payments for a sample of single-family homes with active fixed-rate mortgage loans [1]. (Direct data on insurance premiums paid by individual homeowners is not collected systematically over time at a detailed geographic level by state regulators, any federal agency, or the National Association of Insurance Commissioners, necessitating this type of inference to examine national premium trends.)

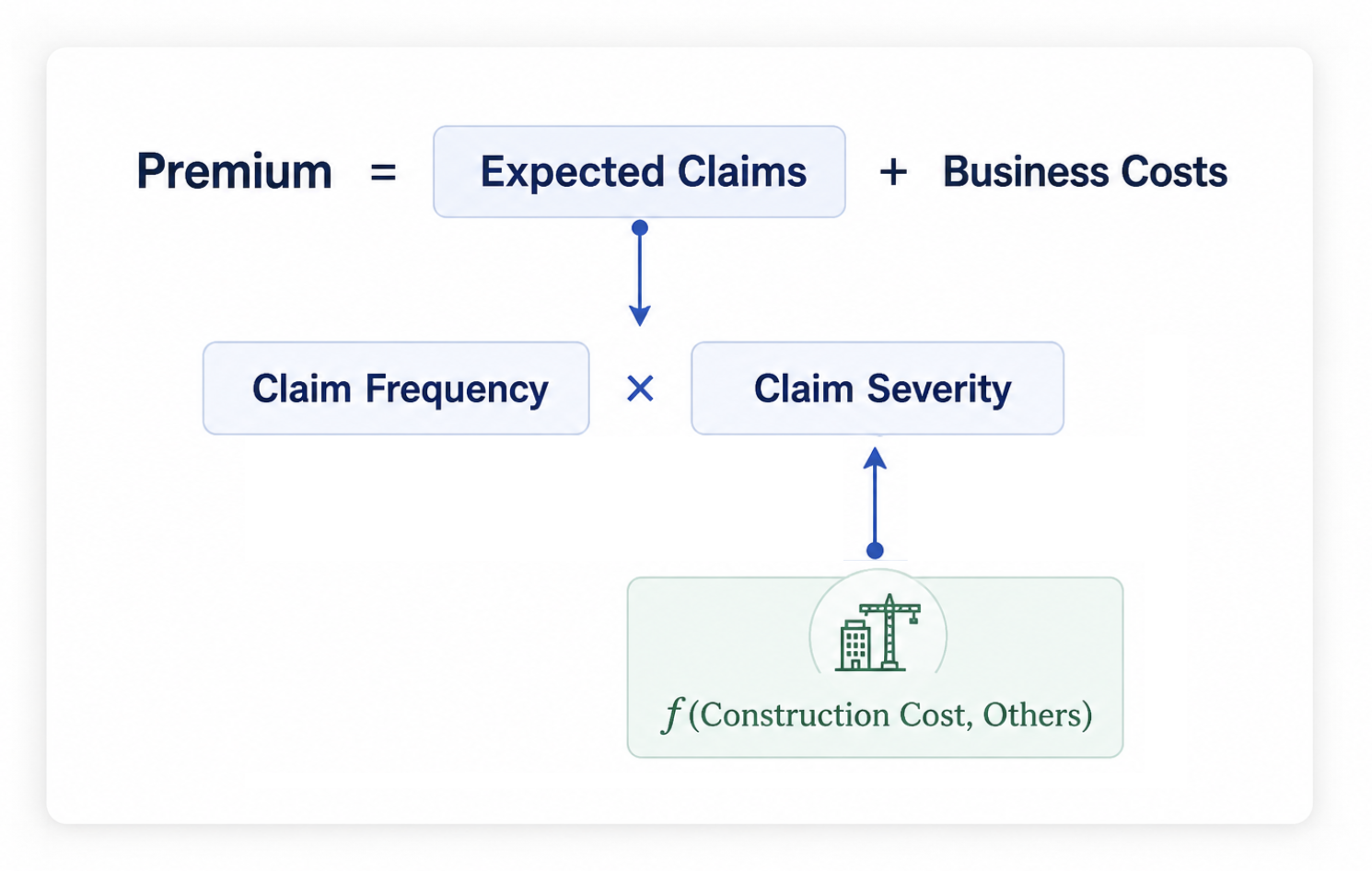

Figure 1: Drivers of Insurance Premiums

In simplified terms, insurance premiums reflect both expected claim payouts, as well as the costs of doing business (see Figure 1). The claims that insurers expect to pay depend on various factors, including but not limited to, the nature of the hazards, characteristics of the property that would influence how much damage is sustained, and features of the insurance contract, such as limits and deductibles. Expected claims are driven by both the frequency of potential payouts and the severity of those payouts. Insurance that is more likely to pay claims (i.e., higher frequency), or that may pay out larger amounts when they occur (i.e., higher severity)—whether because the risk of a covered hazard is greater, the property is not built to withstand perils it faces and is thus more likely to get damaged, or the policy has higher limits and lower deductibles—will generally cost more. In addition, premiums will reflect business costs including marketing and distribution, reinsurance and other risk transfer, underwriting expenses, commissions for agents and brokers, claims handling, as well as some amount for profits and taxes. As such, any factors affecting either expected claim payouts or operating expenses will contribute to changes in property insurance costs.

An often underappreciated driver of premiums is the cost of construction, which is influenced by many macroeconomic factors. In recent years, particularly since the pandemic, construction costs have risen substantially due to a confluence of compounding pressures. Business interruption, shortages of skilled labor, supply chain disruptions, and growing material costs from inflation and trade disputes have led to higher costs to rebuild. Between 2019 and 2024, construction costs have risen by over 40% (see Figure 2), with a double-digit annual growth from 2020 to 2022—a trend that hasn’t been seen since 1981 [2]. As shown in the Figure, since 2019, construction cost inflation has grown more than general inflation. Concern remains that current trade policies, such as tariffs, immigration policies, and ongoing conflict could continue to add inflationary pressure that will continue to increase construction costs in the near-term.

Rising construction costs shift the loss distribution towards larger payouts for insurers, pushing more claims toward policy limits. This directly raises the expected claim severity, or in other words, the average size of claims when losses occur. To maintain their financial position, insurers, therefore, will need to adjust premiums to account for higher reconstruction expenses, leading to increased insurance costs for policyholders. As seen in Figure 2, property insurance costs have tracked more closely with construction cost inflation than with general CPI inflation. When insurance premiums are adjusted for the cost of construction, the increases from 2019 to 2024 are less severe, at 7.5% (versus 52% in unadjusted terms).

This is also illustrated in the maps below, which again show that premium increases have generally been less pronounced once accounting for the growth in construction costs. There is also considerable variation in premium growth around the country. In some parts of the country, such as in Florida, Louisiana, parts of the plains, and northern California, insurance premiums have risen more than construction inflation. However, in some other places, such as parts of New York and Texas, insurance premiums have not kept up with increasing costs of construction. Note that construction inflation may vary by geography as well, which won’t be fully captured with the national construction inflation data we use here for adjustment. For instance, following major disasters that destroy a substantial number of structures in the same area, the demand for rebuilding can exceed supply, pushing construction costs even higher. In such cases where construction inflation is tied to region-specific disaster risk, the real increase in insurance costs may be smaller than what is depicted in the maps.

Much of this remaining variation in premiums could be attributed to growing risks of extreme weather coupled to a building stock that has not been upgraded to reflect our new climate reality. In some regions, claims may be occurring more frequently as weather-related events such as convective storms and hail events become increasingly common on a warming planet. In other cases, weather-related extremes are expected to become more intense when they occur—such as with stronger hurricanes or more destructive wildfires. This can increase the extent of property damage, shifting insured losses toward larger payouts even if reconstruction costs remain unchanged. Together, increases in both the frequency and severity of disasters can contribute to faster premium growth. Of course, insurance price increases can also be constrained by state rate regulations, which aim to protect consumers by restricting how much insurers can raise their rates. In the extreme, however, if regulators do not allow price increases carriers believe are necessary, they may begin to withdraw from the market, a dynamic that has been occurring in high-risk areas of California.

To manage the growing risks of extreme weather events, many insurers transfer a portion of the risk—particularly those at the far tail with extremely low probability but high severity—to the international market through reinsurance. Yet, reinsurance costs are similarly affected by construction inflation: As the cost of construction rises, the overall losses scale up, increasing the expected payouts from reinsurers to ceding insurers that transfer the risk. Therefore, construction costs can be an underlying factor impacting both the primary insurance and property reinsurance markets, as well.

It is worth noting that construction inflation is typically not immediately reflected in insurance pricing. It can take time for such changes to work through the insurance system, largely due to the renewal cycles of insurance and reinsurance contracts, as well as regulatory requirements in some states that may delay rate approvals. As such, the heightened inflationary pressures from construction costs experienced between 2020 and 2022, for example, have likely been gradually felt in the years that followed.

While this post highlighted the influence of construction costs, not discussed in this blog in detail are other major drivers of premiums for U.S. homeowners, including shifting hazard costs, the state regulatory environment, coverage choices, and shifts in the composition of the market [3]. We will delve into some of these topics in greater detail in our next blog post, exploring their nuanced roles in the future of property insurance costs for individuals.

Endnotes

[1] Property insurance premiums from Keys and Mulder (2025) are inferred from mortgage escrow payments as: Property Insurance = Total Escrow Payment − Mortgage Principal − Mortgage Interest − Taxes − Mortgage Insurance.

[2] Calculation using U.S. Construction Price Index for single-family houses under construction from U.S. Census Bureau and U.S. Department of Housing and Urban Development.

[3] Another potential factor, which is somewhat data-related, is the potential change in the profile of mortgage borrowers over the years used to infer property insurance premiums, which may partly explain the differences in premium trends in certain areas as noted in the 2026 GAO report.